Ontario Car Insurance Calculator

Calculate your Ontario car insurance estimates from leading insurance providers in one go

How to get the cheapest Ontario car insurance quote

Get multiple Ontario car insurance quotes in the time it takes to get just one

Enter Your Postal Code

Start with your postal code to begin!

Enter Driver Details

Tell us a little bit about your vehicle, driving & car insurance history.

Compare Your Quotes

Compare your car insurance quotes from more than 50 top insurance companies.

Pick Your Policy

Pick the insurance policy that's right for you to connect directly with the insurance professional of your choice.

Content Manager

What is a car insurance calculator?

A car insurance calculator helps you find the best insurance coverage for your vehicle and any other additional coverage that you may need to add to your insurance policy. InsuranceHotline.com’s car insurance calculator lets you save money by finding the best Ontario car insurance rates from our network of leading insurance providers.

Our car insurance calculator will list available car insurance quotes from multiple providers. Here’s why else you should try InsuranceHotline.com’s car insurance calculator:

- It only takes a few minutes to apply for quotes.

- You can use it anytime and anywhere.

- Ontario calculator users save an average of $890* per year.

How to use our car insurance calculator

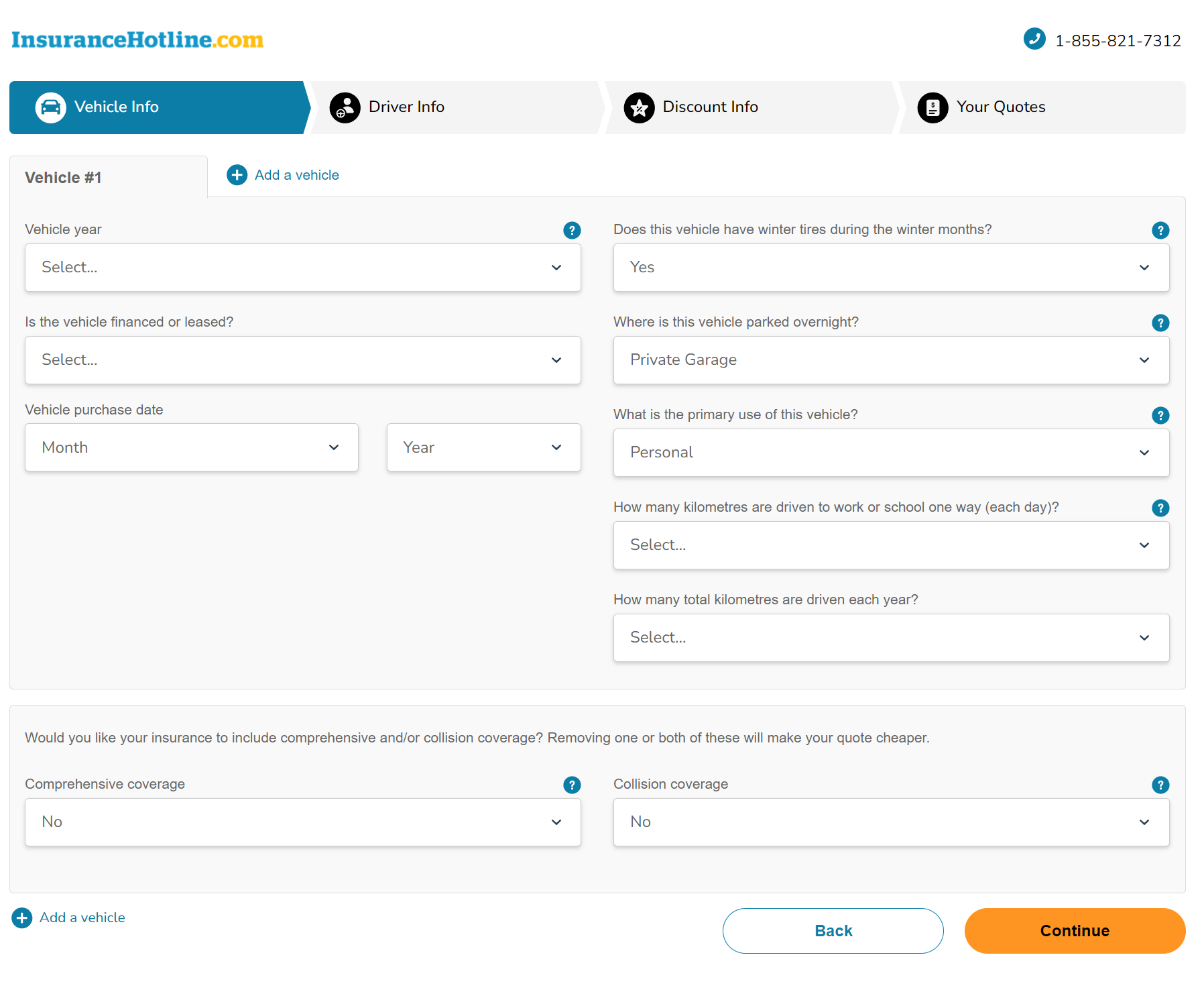

Tell us about your vehicle

Start by sharing some information about your car, including the year of the vehicle, the make, the year it was purchased, and whether you're financing or leasing it. You can add as many vehicles as you would like to insure.

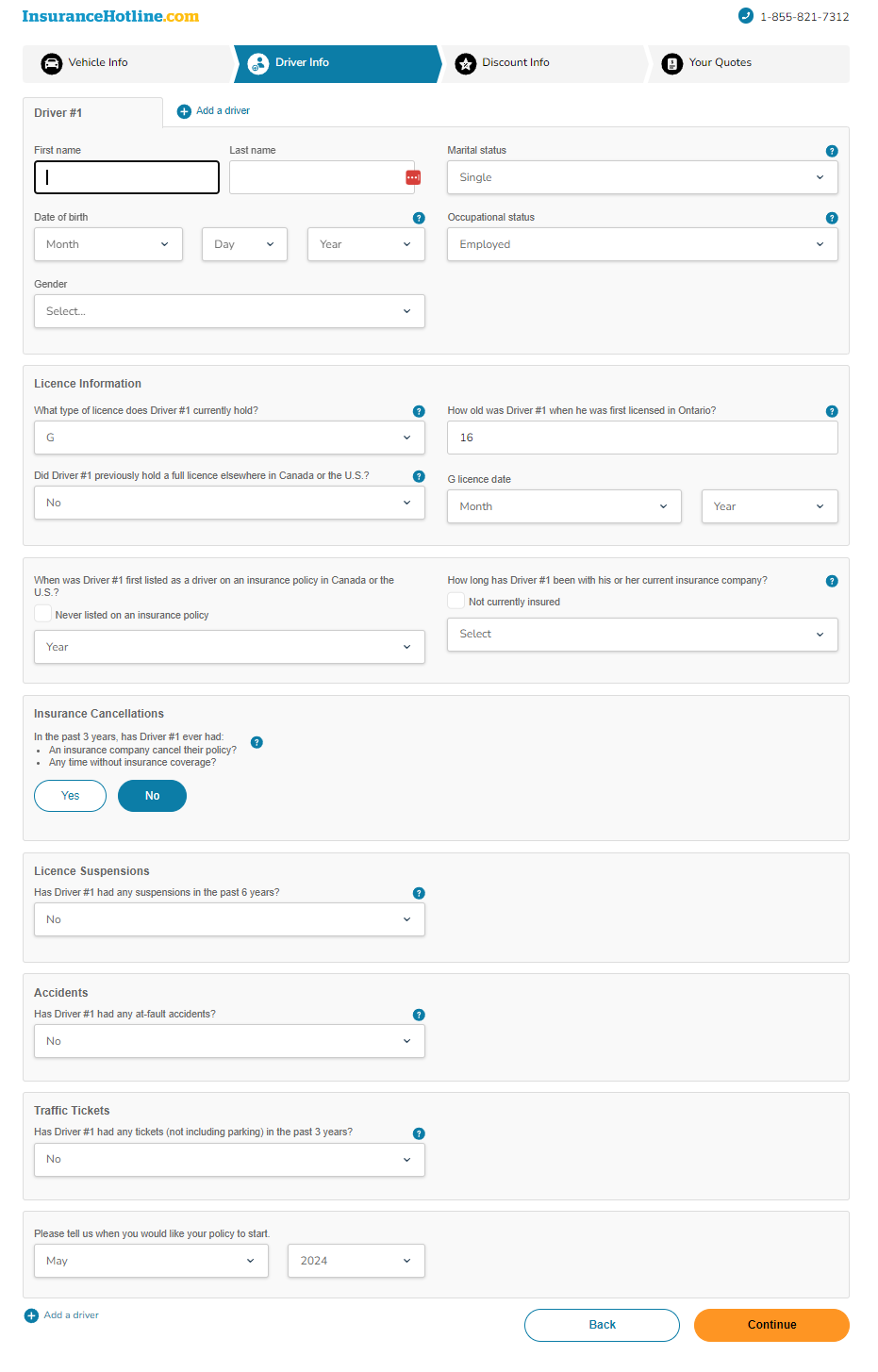

Add driver information

Who drives your car? Tell us who the main drivers will be. Add the licensing information required by the calculator, any accident history, traffic tickets, and when you’d like the policy to start.

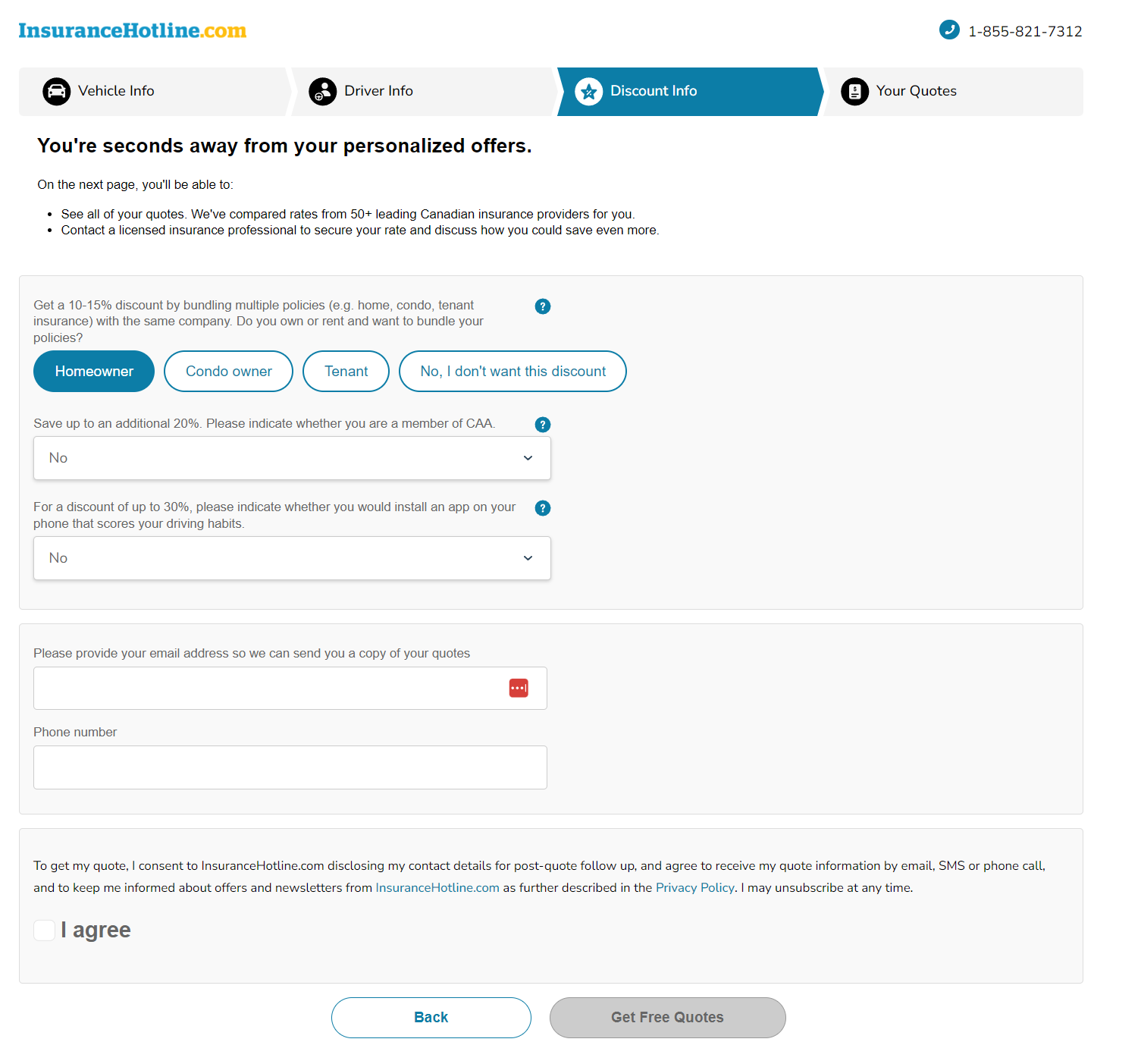

Discount information

At this point you are just one step away from seeing your quotes. If you are a homeowner, you can bundle your auto and home insurance and get a discounted quote. By bundling your insurance, you can get a 10-15% discount with the same company.

See your quote

It’s the moment you’ve been waiting for. Once you input all the information, we will show you the best available quote. InsuranceHotline.ca will connect you with the car insurance provider and help you secure your quote instantly.

Ontario mandatory and optional auto insurance coverage

Learn which coverages you need by law and which ones you can add for a boost. Then compare insurance companies against each other to find your cheapest premium.

| Insurance type | Mandatory coverage | Optional/ Additional Coverage |

|---|---|---|

| Third-Party Liability | $200,000 minimum. Provides coverage in the event of a lawsuit resulting from an accident where you are at fault. | Coverage can be increased to $500,000, $1 million, or $2 million, with up to $2 million limit. |

| Uninsured Automobile Insurance | Provides up to $200,000 in coverage if you are injured or killed by an uninsured driver, or if your vehicle is damaged as a result of a hit-and-run by an unidentified, uninsured motorist. | Family Protection Coverage is an optional coverage that includes additional coverage of up to $1 million in the case of a hit-and-run by an uninsured motorist. |

| Statutory Accident Benefits | Provides coverage if you are injured in an accident, regardless of who is at fault. Covers medical expenses that aren’t covered by OHIP. | Coverage limits can be increased. |

| Direct Compensation-Property Damage (DC-PD) | Optional | DCPD is included in all standard insurance policies, but Ontario drivers can apply to remove it. DCPD pays to repair or replace your car if you're in a collision where the other driver is at fault. You lose this coverage by removing DCPD, as well as your ability to sue the other driver for repairs. |

| Collision Coverage (Also Upset Coverage) | Optional | Covers the costs of repairing or replacing your vehicle following a collision with another vehicle, an object, or property. |

| Comprehensive coverage | Optional | Covers damages caused by named perils identified under the Specified Perils coverage, as well as losses from other perils like falling or flying objects, theft, fire, hail, windstorms, missiles, and vandalism. |

| Specified Perils Coverage | Optional | Covers damages caused by named perils such as theft, attempted theft, explosions, natural disasters like fire, lightning, windstorm, hail, rising water, earthquakes, and other perils specified in your policy. Specified perils do not cover damages due to vandalism, breakage of glass, etc. |

| All-Perils Coverage | Optional | Combines collision/upset and comprehensive coverage. Also, provides additional protection if a household member or an employee steals your vehicle. |

| OPCF 20: Coverage for Transportation Replacement | Optional | Covers the cost of your transportation replacement and rental car insurance if you were to get into a car accident or if your vehicle is stolen. |

| OPCF 27: Liability for Damage to Non-Owned Automobile(s) | Optional | Covers if you damage a borrowed or rental vehicle. The coverage limit is usually around $25,000 to $50,000. |

| OPCF 39: Accident Waiver/Forgiveness | Optional | Protect your premium from rising when you have your first at-fault accident. |

| OPCF 16: Suspension of coverage | Optional | This allows you to suspend your insurance coverage for 30 days or more during periods when you aren't using the car. |

| OPCF 43: Waiver of depreciation | Optional | Ensures your insurance company won't factor in depreciation when settling a claim; you will receive the amount you initially paid for the car. |

| OPCF 44R: Family protection coverage | Optional | Ensures your costs are covered if you and your family are involved in an accident with a driver with less liability insurance than you. This endorsement will cover the remainder. |

| OPCF 13C: Limited glass | Optional | For a lower premium, you can limit or exclude any coverage for glass damage that might've been in your policy. |

| OPCF 40: Fire and theft deductible | Optional | Adds a deductible (an amount you must pay before your insurance company chips in funds) for a theft or fire damage claim. |

Customizing your car insurance coverage

Ontario drivers and vehicle owners are required by law to have auto insurance. If you drive a car without insurance, both the driver and vehicle owner will be subject to fines according to the law. Fines for vehicle owners, lessees and drivers who do not carry valid auto insurance can range from $5,000 to $50,000 and on top of that your driver’s licence can be suspended and your vehicle impounded if you drive without valid auto insurance.

Ontario drivers are subject to a “no-fault" auto insurance system, which means if you are involved in an accident, you will have to deal with your own insurance company. You do not have to pursue the at-fault driver for compensation.

As a result, it is important to customize your car insurance coverage according to your needs. To make sure your auto quote is accurate and tailored to your driving needs, we’ll ask some questions about your car and driving history. Here’s why we ask for the following details:

- General vehicle information – Your vehicle type, make, model and other details can help determine the cost of repair if involved in an accident. For instance, repairing a luxury vehicle like a Porsche or Tesla would be more expensive than repairing a damaged Honda or Subaru.

- Where is the vehicle parked overnight? – In order to determine the probability of theft, the insurance provider must know if your car is parked in a safe and secured garage or on the street. A car is more prone to theft if parked on the driveway or street compared to a car parked in a secure garage in a home. Your quote would change depending on how prone the car is to auto theft. With increasing cases of auto theft in Ontario, insurance providers are taking extra measures to ensure the insurance premium is charged accordingly.

- Primary use of the vehicle and number of kilometers driven each year – A car used to drive kids from home to school and back or just doing groceries once a week is less likely to be in an accident compared to a vehicle that is used to drive to work 200 km a day on a highway every week. The purpose for which your car is used will help your insurance provider anticipate damages in case of an accident.

- Comprehensive and collision coverage – In addition to the standard policy coverage, you may also buy optional coverage for loss or damage to your vehicle if involved in an accident. Comprehensive coverage pays for losses including perils listed under specified perils coverage, including falling or flying objects, missiles and vandalism. Collision or upset coverage pays for losses caused when an insured vehicle is involved in a collision with another object like a trailer or any object in or on the ground, including another vehicle, or rolls over. Choosing these additional coverages will impact your quote.

- Your personal information – The calculator requires you to share your personal information like age, marital status and driver’s licence type as these factors impact your licence. An insurance quote for a 19-year-old new driver would be significantly higher than a 35-year-old driver with a clean driving history as the former is more likely to be involved in an accident due to lack of experience.

- Driving record – Driving convictions, especially licence suspension, at-fault accident, traffic tickets, can impact your insurance, so make sure you provide this information to the insurance company for all the drivers listed on the vehicle. Providing incorrect or false information about a driver or vehicle can lead to the insurance provider declining to issue you a policy.

Car insurance discounts available in Ontario

Insurance providers offer a wide variety of discounts that can help drivers save money on policy. Some insurance companies lower insurance premiums if you are insuring multiple vehicles on the same policy or bundling home and auto insurance into one policy. Discounts are also available for new drivers who have taken defensive driving courses from registered driving schools. Here are a few discount options that will help you save some bucks on premium:

- Driver training discount – Some insurance companies offer a discount to new drivers who have completed a certificate course from a government-approved driving school.

- Graduated license discount – Ontario’s graduated licensing program gives new drivers time to gain driving experience over time. New drivers move up from a G1 to a G2, and finally to a G licence. Each time a driver advances to a new licence level, they get a discount of 10%, provided they don’t have a driving offence or an at-fault accident on their record. The reduction is applicable for one year.

- Group discount or group rates – Insurance providers have discounted group rates for alumni of a participating university, members of a union or professional or occupational association, and certain non-profit associations.

- Mature driver discount – Ontario drivers over the age of 50 with good driving records and no convictions may be eligible for a mature driver discount.

- Multi-policy discount – Insurance companies may offer a discount from 5% to 15% if you purchase your vehicle and home insurance from the same company.

- Multi-vehicle discount – If you own more than one vehicle and want to insure them with one company, you may be eligible for a discount between 5% to 15%.

- Renewal discount – At renewal, insurance companies reduce your rate if you have a clean record (no at-fault accidents or convictions) and have been with the same company for several years. The reduction can range from 5% to 20%.

- Retiree discount – Most providers have a discount for retirees that range from 5% to 15% off your premium for accident benefits coverage if you meet certain criteria.

- Winter tires discount – You must reach out to your insurance provider to ask for a discount if you install winter tires on your vehicle. All insurers offer this discount.

- Other discounts – Some other factors that make you eligible for a discount include low yearly mileage, security and anti-theft system installed in your vehicle and any other system that makes your car more secure and safe to drive.

Get your cheapest car insurance estimate using our Ontario car insurance calculator

No matter where you live, what you drive, or your history, there are things you can do to lower your rate. Here are our top tips.

1. Compare annually. Using a car insurance calculator to get estimates from multiple insurance companies is an effective, efficient way to shave hundreds of dollars off your annual insurance bill instantly. When using the car insurance calculator, you want to be as accurate as possible when entering information to receive the most accurate quotes. The more precise you are, the more precise your quotes will be.

2. Bundle your insurance. Choose the bundle option if you're open to having your home and car insurance with the same provider. It will help you save even more!

3. Try a telematics program. Choose the telematics option when filling out the calculator form. Telematics technology lets car insurance companies monitor how much and how well you drive by installing a GPS device through your cars onboard computer. The insurance companies supply the device. It qualifies you to enroll in pay-as-you-go auto insurance programs or receive additional discounts for safe driving behaviour.

4. Take advantage of memberships. Insurance companies offer individual and group discounts and ones for driving an eco-friendly car. Other discounts include ones for bundling car and home insurance, making regular payments (be it a lump sum or monthly automated ones), buying a new vehicle, installing anti-theft devices, taking driver training classes, and even being a good student (if you're enrolled in post-secondary). Cheaper rates are also possible through group insurance programs offered by professional organizations, workplaces, or your alma mater

5. Adjust your deductible. Your deductible also impacts your rates. The deductible is the amount you pay in the event of a claim. Most insurers set deductibles at $500, but you may get a lower premium if you raise your deductible to $1,000. If you increase your deductible, ensure you have enough money to cover it.

6. Use winter tires. The specially designed treads on winter tires push away water, snow, and ice. Driving on them between November 1 and April 1 could deliver a discount of up to 5% on your premium.

Find out how much you could be saving with InsuranceHotline.coms car insurance calculator today.

We've got hundreds of 5 star reviews

2,351 reviews on TrustPilot. See some of the reviews here.

Massimo D

G WILLIAMS

Janice

colvin smith

Raj Kang

Kathryn

Shiva

Josephine Liagarpao

Hoang Tran

Jmaes

Bruce

Goodness Okoroma

Cecil Pickering

Tracey

Farhad Hamraz

Ben Yang

Tai Lu

*Shoppers in Ontario who obtained a quote on InsuranceHotline.com from January to December 2023 saved an average of $890 per year. The average savings amount represents the difference between the shoppers’ average lowest quoted premium and the average of the second and third-lowest quoted premiums generated by InsuranceHotline.com.